Modelling Historical Data for an All-In-One Fund ETF#

VDAL is a new all-in-one fund ETF created by Vanguard, brought out by popular demand for a VDHG ETF alternative without the bonds. Although this new ETF is very promising, its historical data is limited as it was only recently released. Through analysis of its underlying holdings, we can predict and extend this data decades into the past.

Note

Because this process is quite long and technical, you can skip ahead to the final result by navigating through the sidebar. The rest of the article (which explains methodology and provides all code) is optional and is not designed to be read on mobile.

Packages, configurations, and functions used#

Packages#

import datetime as dt

import numpy as np

import pandas as pd

import pandas_datareader.data as web

import matplotlib.pyplot as plt

import matplotlib.ticker as mtick

import matplotlib.patches as patches

import matplotlib.colors as mcolors

import yfinance as yf

from sklearn.metrics import r2_score

from sklearn.linear_model import LinearRegression

from matplotlib.ticker import LogLocator, FuncFormatter

from matplotlib.ticker import ScalarFormatter

Configurations#

plt.rc("figure", labelsize="x-large", autolayout=True, figsize=(4, 3))

Functions#

def set_offset_from_first_valid_index(df, col, offset, y):

first_valid_index = df[col].first_valid_index()

offset_from_first_valid_index = df[col].index.get_loc(first_valid_index) + offset

df.loc[df.index[offset_from_first_valid_index], col] = y

def normalised(x):

x = x.ffill().dropna().pct_change(fill_method=None)

x = (1 + x).cumprod()

x.iloc[0] = 1

return x

def normalise_stock_performance(df, rebase_stock=None):

# default to youngest stock

if rebase_stock == None:

rebase_stock = (

df.apply(lambda x: x.first_valid_index())

.sort_values(ascending=False).index[0]

)

df = df.copy()

# normalise each column individually

for stock in df.columns:

df[stock] = normalised(df[stock])

# scale stocks relatively

rebase_date = df[rebase_stock].first_valid_index()

for stock in df.columns:

rebase_value = df[stock].loc[rebase_date]

df[stock] = df[stock] / rebase_value

return df

def plot_correlation(df, actual, predicted, actual_label=None, predicted_label=None):

if actual_label == None:

actual_label = actual

if predicted_label == None:

predicted_label = predicted

plot_df = df[[actual, predicted]]

plot_df = plot_df.dropna()

plot_df = normalise_stock_performance(plot_df)

y1 = (plot_df.pct_change(fill_method=None) + 1).dropna()

y1 = y1.rolling(30).apply(lambda x: x.prod()).dropna()

y1 -= 1

y_true = y1[actual]

y_pred = y1[predicted]

r2 = r2_score(y_true, y_pred)

x2 = np.array(y_true).reshape(-1, 1)

y2 = np.array(y_pred)

model = LinearRegression()

model.fit(x2, y2)

x_fit = np.linspace(x2.min(), x2.max(), 100).reshape(-1, 1)

y_fit = model.predict(x_fit)

slope = model.coef_[0]

intercept = model.intercept_

fig, axs = plt.subplots(1, 2, figsize=(8, 3))

axs[0].plot(plot_df[actual])

axs[0].plot(plot_df[predicted])

axs[0].set_title("Total Return (%)")

axs[0].legend([actual_label, predicted_label])

axs[0].yaxis.set_major_formatter(FuncFormatter(lambda x, _: f"{100 * (x - 1):.0f}%"))

axs[1].plot([y_true.min(), y_true.max()], [y_true.min(), y_true.max()])

axs[1].plot(x_fit, y_fit)

axs[1].scatter(y_true, y_pred, s=1, color=mcolors.TABLEAU_COLORS["tab:orange"], zorder=2)

axs[1].text(0.1, 0.9, f"R2: {r2:.2f}", transform=axs[1].transAxes)

axs[1].text(0.1, 0.8, f"y = {slope:.2f}x + {intercept:.2f}", transform=axs[1].transAxes)

axs[1].set_title(f"30-Day Returns: {actual_label} vs. {predicted_label}")

axs[1].xaxis.set_major_formatter(mtick.FuncFormatter(lambda x, _: f"{100 * x:.0f}%"))

axs[1].yaxis.set_major_formatter(mtick.FuncFormatter(lambda x, _: f"{100 * x:.0f}%"))

fig.autofmt_xdate()

plt.show()

Downloading and preparing the data#

stocks = ["VDAL.AX", "VDHG.AX"]

stocks += ["VAS.AX", "VGS.AX", "VGAD.AX", "VISM.AX", "VGE.AX"]

stocks += ["IOO.AX", "STW.AX", "IEM.AX"]

stocks += ["IOO", "EWA", "EEM"]

stocks += ["^SP500TR"]

df_orig = yf.download(stocks, period="max", group_by="ticker", auto_adjust=False)

aud_usd = web.DataReader("DEXUSAL", "fred", start=dt.datetime(1900, 1, 1))

df = df_orig.copy()

df = df.xs("Adj Close", axis=1, level=1)

df["AUDUSD=X"] = aud_usd

df["USDAUD=X"] = 1 / df["AUDUSD=X"]

Looking at VDAL’s holdings#

From VDAL’s fact sheet, we can see its target asset allocation is as follows:

Asset |

Target (%) |

|---|---|

Australian Shares |

40 |

International Shares |

29.5 |

International Shares (Hedged) |

18 |

International Small Companies |

7 |

Emerging Markets Shares |

5.5 |

We can look at various ETFs and indices to model this allocation. However, as you will soon see, the further into the past we go, the more we need to compromise on accuracy. To get the best of both worlds, we will create multiple models with varying trade-offs between accuracy and length. Afterwards, we can then append them all together in order of accuracy.

Model A: Weighted Return of Component ETFs#

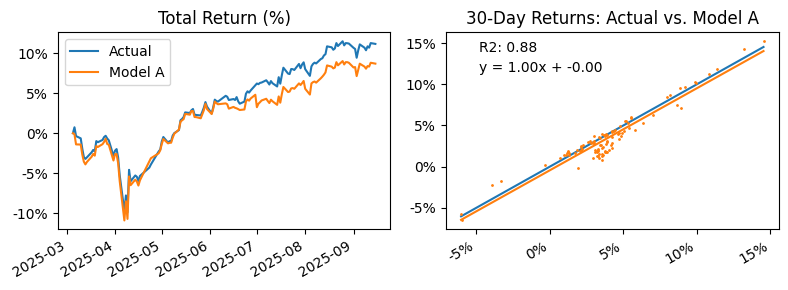

For our first model, let’s look at the actual holdings of VDAL. The above allocation specifically corresponds to five Vanguard ETFs: VAS, VGS, VGAD, VISM, and VGE. All five of these ETFs are much older than VDAL, allowing us to highly accurately model VDAL prior to its inception date.

Model A will be created through the combined return of the five component ETFs, weighted accordingly by their target allocations:

df["model_a"] = (

0.40 * df["VAS.AX"].pct_change(fill_method=None) +

0.295 * df["VGS.AX"].pct_change(fill_method=None) +

0.18 * df["VGAD.AX"].pct_change(fill_method=None) +

0.07 * df["VISM.AX"].pct_change(fill_method=None) +

0.055 * df["VGE.AX"].pct_change(fill_method=None)

)

df["model_a"] = (df["model_a"] + 1).cumprod()

set_offset_from_first_valid_index(df, "model_a", -1, 1)

plot_correlation(df, "VDAL.AX", "model_a", "Actual", "Model A")

Model A has a strong correlation to the original, giving high confidence that the predicted data past VDAL’s inception date is reliable.

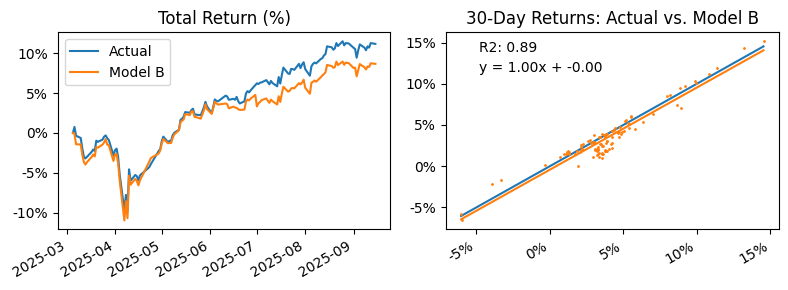

Model B: Absorbing VISM into VGS#

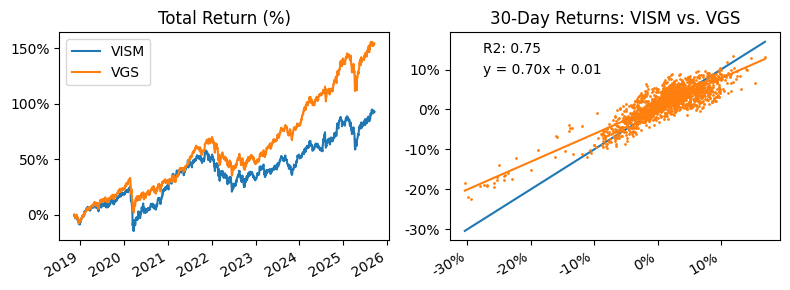

When looking at the five component ETFs, VISM’s inception date is significantly later than the rest. If we were to substitute VISM in our next model, we can extend the data a further four years.

I chose to absorb VISM (International Small Cap) into VGS (International Large/Mid Cap), justifying that the two should perform similarly to due to their similar regional exposure. Additionally, because VISM only makes up a small fraction of the total allocation, any minor difference caused by this substitution should turn negligible.

Let’s first test our assumptions by comparing the two components:

plot_correlation(df, "VISM.AX", "VGS.AX", "VISM", "VGS")

As thought, VISM and VGS share a moderate correlation.

Let’s now test the effect of this substitution in model B:

df["model_b"] = (

0.40 * df["VAS.AX"].pct_change(fill_method=None) +

(0.295 + 0.07) * df["VGS.AX"].pct_change(fill_method=None) +

0.18 * df["VGAD.AX"].pct_change(fill_method=None) +

0.055 * df["VGE.AX"].pct_change(fill_method=None)

)

df["model_b"] = (df["model_b"] + 1).cumprod()

set_offset_from_first_valid_index(df, "model_b", -1, 1)

plot_correlation(df, "VDAL.AX", "model_b", "Actual", "Model B")

We can see that our assumptions were correct. No significant change in correlation was observed from this substitution.

Model C: Substituting Components with Older ETFs#

Similarly, further data can be obtained by substituting components with entirely different older alternatives that have similar regional exposure:

VGS (International Large/Mid Cap) with IOO (International Top 100).

VAS (Australian Shares) with STW (Australian Top 200)

VGE (Emerging Markets Shares) with IEM (Emerging Markets Shares)

VGAD (International Large/Mid Cap Hedged) is a little bit more tricky as there is no simple currency hedged replacement. We can do our best by modelling a hedged version of IOO by tying it to the performance of AUD/USD:

df["IOO_hedged"] = df["IOO.AX"] * df["AUDUSD=X"]

Now let’s look at how each component is correlated to their corresponding substitution:

plot_correlation(df, "VGS.AX", "IOO.AX", "VGS", "IOO")

plot_correlation(df, "VGAD.AX", "IOO_hedged", "VGAD", "IOO Hedged")

plot_correlation(df, "VAS.AX", "STW.AX", "VAS", "STW")

plot_correlation(df, "VGE.AX", "IEM.AX", "VGE", "IEM")

---------------------------------------------------------------------------

IndexError Traceback (most recent call last)

Cell In[15], line 1

----> 1 plot_correlation(df, "VGS.AX", "IOO.AX", "VGS", "IOO")

2 plot_correlation(df, "VGAD.AX", "IOO_hedged", "VGAD", "IOO Hedged")

3 plot_correlation(df, "VAS.AX", "STW.AX", "VAS", "STW")

Cell In[6], line 10, in plot_correlation(df, actual, predicted, actual_label, predicted_label)

8 plot_df = df[[actual, predicted]]

9 plot_df = plot_df.dropna()

---> 10 plot_df = normalise_stock_performance(plot_df)

12 y1 = (plot_df.pct_change(fill_method=None) + 1).dropna()

13 y1 = y1.rolling(30).apply(lambda x: x.prod()).dropna()

Cell In[5], line 13, in normalise_stock_performance(df, rebase_stock)

11 # normalise each column individually

12 for stock in df.columns:

---> 13 df[stock] = normalised(df[stock])

15 # scale stocks relatively

16 rebase_date = df[rebase_stock].first_valid_index()

Cell In[4], line 4, in normalised(x)

2 x = x.ffill().dropna().pct_change(fill_method=None)

3 x = (1 + x).cumprod()

----> 4 x.iloc[0] = 1

6 return x

File ~/.local/lib/python3.12/site-packages/pandas/core/indexing.py:908, in _LocationIndexer.__setitem__(self, key, value)

906 key = self._check_deprecated_callable_usage(key, maybe_callable)

907 indexer = self._get_setitem_indexer(key)

--> 908 self._has_valid_setitem_indexer(key)

910 iloc = self if self.name == "iloc" else self.obj.iloc

911 iloc._setitem_with_indexer(indexer, value, self.name)

File ~/.local/lib/python3.12/site-packages/pandas/core/indexing.py:1646, in _iLocIndexer._has_valid_setitem_indexer(self, indexer)

1644 elif is_integer(i):

1645 if i >= len(ax):

-> 1646 raise IndexError("iloc cannot enlarge its target object")

1647 elif isinstance(i, dict):

1648 raise IndexError("iloc cannot enlarge its target object")

IndexError: iloc cannot enlarge its target object

All substitutes have strong correlations with their original. Let’s now put it together and construct model C:

df["model_c"] = (

0.40 * df["STW.AX"].pct_change(fill_method=None) +

(0.295 + 0.07) * df["IOO.AX"].pct_change(fill_method=None) +

0.18 * df["IOO_hedged"].pct_change(fill_method=None) +

0.055 * df["IEM.AX"].pct_change(fill_method=None)

)

df["model_c"] = (df["model_c"] + 1).cumprod()

set_offset_from_first_valid_index(df, "model_c", -1, 1)

plot_correlation(df, "VDAL.AX", "model_c", "Actual", "Model C")

Model C’s correlation remains strong to the original despite the more drastic changes.

Model D: Substituting Components with Older US-based ETFs#

In model C, we dealt only with ETFs available on the Australian exchange. But by extending our search to international exchanges such as the US, we can find even more data.

Because we are now looking at the US exchange, we need to factor in currency fluctuations. Much like how we simulated currency hedging in the previous model, we can do the same here to model each ETF as if on the Australian exchange. We also shift the data by one day to adjust for the time zone difference.

df["EWA_USDAUD"] = (df["EWA"] * df["USDAUD=X"]).shift(1)

df["IOO_USDAUD"] = (df["IOO"] * df["USDAUD=X"]).shift(1)

df["EEM_USDAUD"] = (df["EEM"] * df["USDAUD=X"]).shift(1)

plot_correlation(df, "VGS.AX", "IOO_USDAUD", "VGS", "IOO")

plot_correlation(df, "VGAD.AX", "IOO", "VGAD", "IOO ")

plot_correlation(df, "VAS.AX", "EWA_USDAUD", "VAS", "EWA")

plot_correlation(df, "VGE.AX", "EEM_USDAUD", "VGE", "EEM")

Here the correlation score begins to suffer, though still remains relatively strong. Let’s now construct model D:

df["model_d"] = (

0.40 * df["EWA_USDAUD"].pct_change(fill_method=None) +

(0.295 + 0.07) * df["IOO_USDAUD"].pct_change(fill_method=None) +

0.18 * df["IOO"].pct_change(fill_method=None) +

0.055 * df["EEM_USDAUD"].pct_change(fill_method=None)

)

df["model_d"] = (df["model_d"] + 1).cumprod()

set_offset_from_first_valid_index(df, "model_d", -1, 1)

plot_correlation(df, "VDAL.AX", "model_d", "Actual", "Model D")

Model E: Removing Emerging Markets#

At this point we have exhausted possible substitutions. The next step to extend the data then is to simply look at removing the younger components. By removing EEM and absorbing its allocation into the remaining components, model E extends the data a further three years:

df["model_e"] = (

0.40/0.945 * df["EWA_USDAUD"].pct_change(fill_method=None) +

(0.295 + 0.07)/0.945 * df["IOO_USDAUD"].pct_change(fill_method=None) +

0.18/0.945 * df["IOO"].pct_change(fill_method=None)

)

df["model_e"] = (df["model_e"] + 1).cumprod()

set_offset_from_first_valid_index(df, "model_e", -1, 1)

plot_correlation(df, "VDAL.AX", "model_e", "Actual", "Model E")

Model H: The Amalgamation#

Finally, we append each model together in order of their faithfulness to the original allocation:

df["model_h"] = (

df["VDAL.AX"].pct_change(fill_method=None)

.fillna(df["model_a"].pct_change(fill_method=None))

.fillna(df["model_b"].pct_change(fill_method=None))

.fillna(df["model_c"].pct_change(fill_method=None))

.fillna(df["model_d"].pct_change(fill_method=None))

.fillna(df["model_e"].pct_change(fill_method=None))

.fillna(df["model_f"].pct_change(fill_method=None))

)

df["model_h"] = (df["model_h"] + 1).cumprod()

set_offset_from_first_valid_index(df, "model_h", -1, 1)

fig, ax = plt.subplots()

plot_df = df[["model_h"]]

plot_df = normalise_stock_performance(plot_df)

ax.plot(plot_df["model_h"][df["VDAL.AX"].first_valid_index():])

ax.plot(plot_df["model_h"][df["model_a"].first_valid_index():df["VDAL.AX"].first_valid_index():])

ax.plot(plot_df["model_h"][df["model_b"].first_valid_index():df["model_a"].first_valid_index():])

ax.plot(plot_df["model_h"][df["model_c"].first_valid_index():df["model_b"].first_valid_index():])

ax.plot(plot_df["model_h"][df["model_d"].first_valid_index():df["model_c"].first_valid_index():])

ax.plot(plot_df["model_h"][df["model_e"].first_valid_index():df["model_d"].first_valid_index():])

ax.plot(plot_df["model_h"][df["model_f"].first_valid_index():df["model_e"].first_valid_index():])

ax.plot(plot_df["model_h"][df["model_g"].first_valid_index():df["model_f"].first_valid_index():])

ax.set_title("Model H Historical Performance")

ax.legend(["Actual", "A", "B", "C", "D", "E", "F"])

ax.yaxis.set_major_formatter(mtick.FuncFormatter(lambda x, _: f"{100 * (x - 1):.0f}%"))

fig.autofmt_xdate()

plt.show()

Final Results#

We have turned what originally was less than a year of data into something that spans decades long. Below is the final result with reference to the original: